Author: SRCO Business Insights | December 22, 2024

Auditing ensures transparency, accuracy, and compliance in an organization’s financial and operational activities. There are two main categories within the auditing field: Internal Audit and External Audit. While both aim to improve an organization’s financial integrity, they serve different purposes, are conducted by other parties, and focus on various aspects of its processes. This blog will explore the difference between internal audit and external audit report to help businesses better understand their roles and importance.

Internal Audit Overview

What is Internal Audit?

An internal audit is an independent, objective assurance activity designed to add value and improve an organization’s operations. It helps an organization accomplish its objectives by evaluating and improving the effectiveness of risk management, control, and governance processes. Internal audits are conducted by organization employees or by an external firm hired specifically for this role.

Key Objectives of Internal Audit

The primary goals of internal audits include:

- Risk Management: Assessing the risk management framework to ensure it identifies, evaluates, and mitigates risks effectively.

- Internal Control Systems: Ensuring that internal control systems are robust, operational, and compliant with regulatory requirements.

- Compliance: Monitoring adherence to policies, procedures, and laws to prevent fraud, waste, and abuse within the organization.

- Operational Efficiency: Improving business processes, identifying inefficiencies, and recommending corrective actions.

- Fraud Detection: Identifying areas vulnerable to fraud and preventing financial mismanagement.

Features of Internal Audit

- Scope and Focus: The scope of internal audits is broad and includes financial processes and operational, compliance, and IT controls.

- Frequency: Internal audits are continuous, conducted on an ongoing basis, and often cover different departments, functions, or processes.

- Independence: Internal auditors report directly to senior management or the audit committee to ensure independence, although they are part of the organization.

- Internal Relationships: Internal audits work closely with the company’s management team, providing recommendations for improvement based on their findings.

External Audit Overview

What is an External Audit?

An external audit is an independent examination of an organization’s financial statements, typically performed by a third-party firm or auditor. The objective is to provide an opinion on whether the financial statements present an accurate and fair view of the organization’s financial position and comply with accounting standards and regulatory requirements.

External audits are typically required by law for public companies, government entities, and large private companies to ensure transparency for investors, regulators, and other stakeholders. External auditors do not work for the organization they audit, which helps maintain objectivity and impartiality.

Key Objectives of External Audit

The primary goals of an external audit include:

- Financial Statement Accuracy: Ensuring that the organization’s financial statements are free from material misstatements and reflect the company’s financial position.

- Compliance with Regulations: Verifying that the organization complies with accounting standards, tax laws, and other regulatory requirements.

- Audit Opinion: Providing an opinion on whether the organization’s financial statements are presented fairly, in all material respects, by the applicable financial reporting framework (e.g., IFRS or GAAP).

- Public Confidence: Enhancing the confidence of investors, shareholders, creditors, and other stakeholders in the organization’s financial reporting.

Features of External Audit

- Scope and Focus: External audits focus solely on the accuracy and fairness of financial statements, ensuring compliance with accounting principles.

- Frequency: External audits are typically performed annually or quarterly, depending on the company’s needs and regulatory requirements.

- Independence: External auditors are independent of the organization they audit and work for an external auditing firm.

- External Relationships: External auditors report their findings to stakeholders, including shareholders, regulators, and the public.

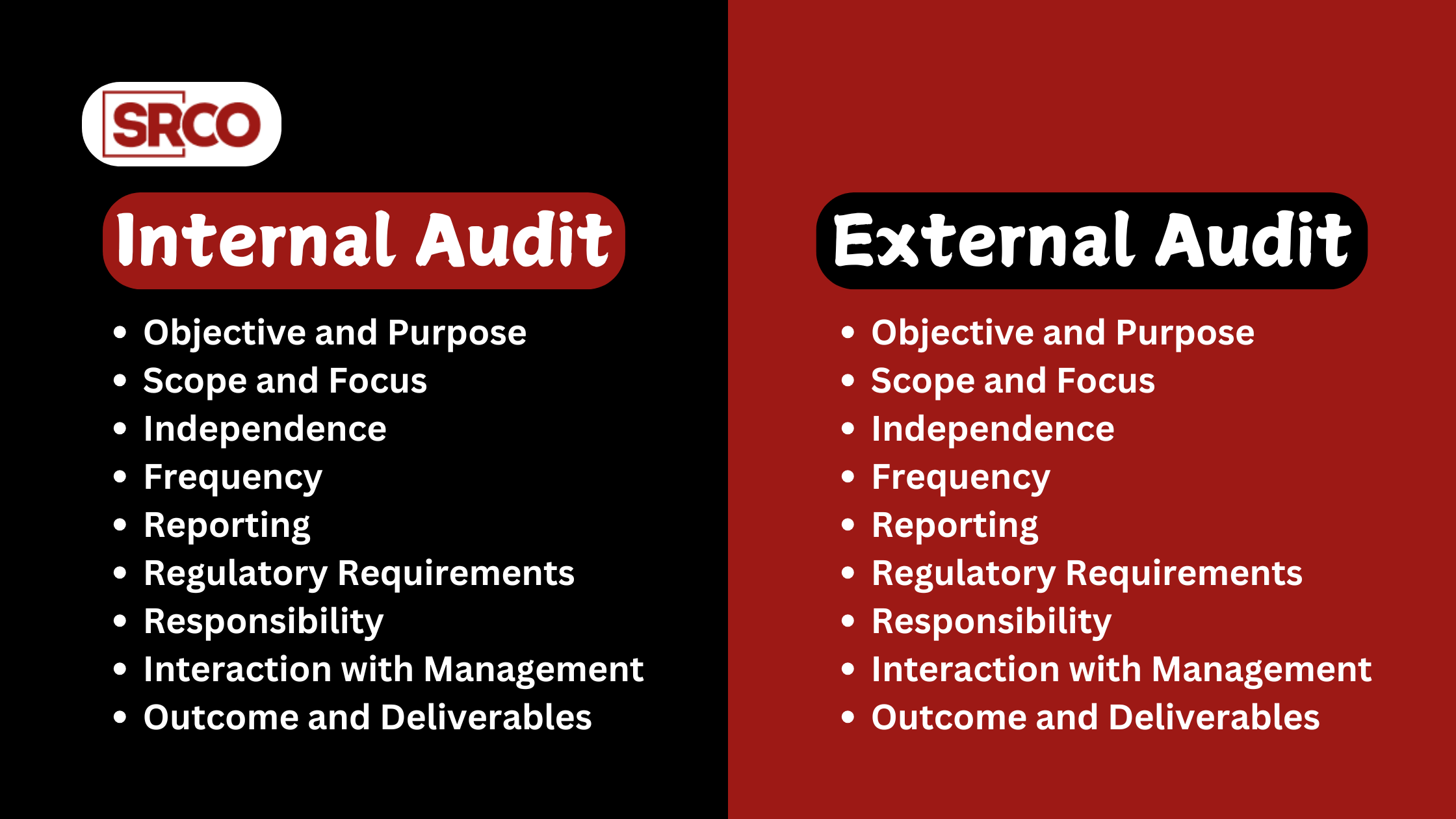

Key Difference Between Internal Audit and External Audit

Understanding the distinctions between internal and external audits is crucial for organizations to meet their financial, operational, and regulatory obligations. Below, we break down the key differences between the two types of audits.

- Objective and Purpose

- Internal Audit: The primary objective of internal audit is to evaluate and improve the effectiveness of internal controls, risk management processes, and governance. It helps an organization improve its operations and mitigate risks by providing insights to management.

- External Audit: The main goal of an external audit is to verify the accuracy and fairness of an organization’s financial statements. External auditors provide an independent opinion on whether the financial statements give an accurate and fair view of the company’s financial position.

- Scope and Focus

- Internal Audit: Internal audits have a broader scope, covering not just financial records but also operational efficiency, compliance, risk management, and internal controls. Internal auditors may review processes across various departments or functions.

- External Audit: The scope of an external audit is narrower and focuses primarily on the organization’s financial statements, ensuring they comply with accounting standards and regulatory requirements.

- Independence

- Internal Audit: Internal auditors are employees of the organization, though they report to the board or audit committee to maintain their independence. Their autonomy is crucial for ensuring unbiased assessments of company operations.

- External Audit: External auditors are entirely independent of the organization being audited. This independence is key to ensuring their audit results are objective and reliable for external stakeholders.

- Frequency

- Internal Audit: Internal audits are usually ongoing and conducted regularly. Depending on the organization’s risk profile and audit plan, they may occur quarterly, biannually, or annually.

- External Audit: External audits are typically conducted once a year, mainly providing an opinion on the year-end financial statements.

- Reporting

- Internal Audit: Internal auditors report their findings to management, including the CEO, CFO, and the audit committee. Their reports are typically used to inform decision-making and guide organizational process improvements.

- External Audit: External auditors report their findings to shareholders, regulators, and the public (in the case of public companies). They provide an audit opinion on whether the financial statements are accurate and fair.

- Regulatory Requirements

- Internal Audit: There are no strict legal requirements for internal audits, but they are often mandated by the organization’s internal policies, corporate governance codes, or industry regulations.

- External Audit: External audits are typically required by law, especially for publicly listed companies, to provide transparency to investors and other stakeholders.

- Responsibility

- Internal Audit: The responsibility for conducting internal audits lies with the organization, typically a dedicated internal audit department or an external service provider.

- External Audit: External audits are conducted by independent third-party audit firms, and the responsibility for the audit opinion lies with the auditing firm.

- Interaction with Management

- Internal Audit: Internal auditors work closely with management, identifying areas for improvement, recommending process changes, and helping to implement improvements.

- External Audit: External auditors have minimal interaction with management during the audit process. They primarily focus on reviewing financial records and may meet with management to clarify issues, but they do not actively work with the company to improve operations.

- Outcome and Deliverables

- Internal Audit: The deliverables of an internal audit include detailed reports, assessments, and recommendations for improving internal controls, risk management, and operational processes.

- External Audit: The deliverables of an external audit include an audit report and an opinion on the fairness and accuracy of the organization’s financial statements.

Which One Should You Choose?

Internal and external audits are essential for an organization but serve different purposes. An internal audit is ideal for organizations looking to improve internal controls, manage risks, and optimize operations. It provides a continuous, proactive approach to strengthening the organization’s internal processes.

On the other hand, an external audit is necessary to ensure that the financial statements comply with accounting standards and regulatory requirements. It assures external stakeholders the accuracy and reliability of the organization’s financial reporting.

Both types of audits are integral for companies looking to maintain operational efficiency, ensure regulatory compliance, and build stakeholder confidence. By integrating the insights and recommendations from internal and external audits, businesses can achieve improved financial transparency, operational effectiveness, and risk management.

Conclusion

Both internal and external audits play critical roles in maintaining an organization’s integrity, transparency, and efficiency. Internal audits focus on enhancing operations, managing risks, and improving controls, while external audits provide an independent opinion on the accuracy and fairness of financial statements. Understanding the key differences between the two can help organizations better navigate their financial and operational challenges and make informed decisions to drive long-term success.

At S. Rahman & Co., we offer internal and external audit services to help organizations like yours stay compliant, optimize operations, and build stakeholder trust. Our team of experienced auditors works closely with your business to ensure that your audit needs are met, providing you with valuable insights for growth and improvement.

If you want to learn more about our auditing services or need expert guidance on managing your organization’s audit processes, please get in touch with us today.

Blogs